A financial crisis-style extended period of austerity after the coronavirus emergency “is not a done deal”, a top economist has said.

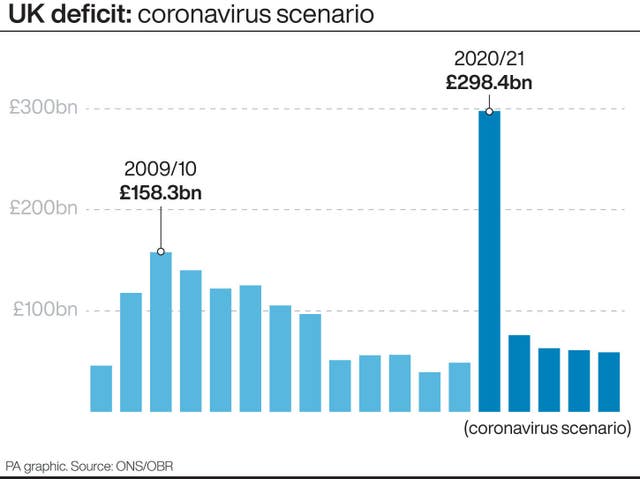

Office for Budget Responsibility (OBR) chairman Robert Chote said reported Government debt of more than £300 billion did not necessarily have to mean years of slashing public expenditure.

Mr Chote also said the UK economy should be over “the worst of it” in terms of the economic hit from the lockdown, and is now entering a recovery phase as the public health restrictions are gradually relaxed.

The economist told the BBC’s Andrew Marr show: “We’re certainly going to see – temporarily – a higher amount of Government borrowing.

“The fact that the level of debt goes up on its own doesn’t necessarily mean you have to have the sort of austerity that followed the financial crisis.

“Much more important to that is whether you have this effect of scarring of the economy. If the economy is permanently smaller then you get permanently less tax revenue.

“Do we come out of this with a much bigger debt interest bill? At the moment it’s relatively cheap for the Government to borrow so hopefully that won’t be too much of a problem.

“Then also there will be political choices coming out of this. Do we want to spend a higher proportion of national income than we went in for example on health and social care?

“All of these things together will shape the fiscal challenge for the Government coming out of this. A post financial crisis-style extended period of austerity is not a done deal.”

Regarding the UK’s economic recovery, Mr Chote said: “People shouldn’t panic in the sense that we know the economy, probably at its worst last month, may have been a third or so smaller than it normally would have been in terms of the output of goods and services and people’s spending.

“But that should be the worst of it and we now go into a period of recovery as the restrictions are loosened.”

Outlining factors critical to the economic health of the UK, he highlighted the pace on which public health restrictions are relaxed, as well as people’s behaviour.

He added: “If you allow people back into the workplace, back into shops, back into restaurants, will they actually go? Will they feel too nervous?”

Separately, Carolyn Fairbairn, director-general of the Confederation of British Industry (CBI), told Sky News that businesses were thinking about protecting furloughed jobs for the future, adding it required a “cautious, careful restart”.

She said: “This week, I think from the business perspective, has been a week of glimmers of light at the end of the tunnel.

“We had the encouragement at the beginning of the week for businesses to get back to work, they are following that putting safety first… but what we are concerned about is the policies need to be co-ordinated across transport, across schools, across the devolved nations.

“If we do not have consensus that will undermine confidence amongst workers, consumers and people in general.”

Dame Carolyn added the idea of health-of-the-nation versus health-of-the-economy was a “false dichotomy”.

She went on: “You cannot have a strong economy without public safety. The worst thing that could happen would be another lockdown. These two objectives go hand in hand.

“We should not be seeing these two things in conflict.”